Part 1: Blockchain Basics

Blockchain, Bitcoin, and Cryptocurrency. Chances are you’ve heard one or all of these word in the last seven days. These three words—as well as the discussion, debate, and speculation that surrounds them—have become hard to escape for even the non-technical. If you work in the technology industry, it becomes nearly impossible to not run across a discussion or debate involving blockchain.

Unfortunately, few people really understand what they are, let alone what they mean or could mean to our technology landscape and the greater world at large, although they dominate our tech conversations and financial news. Even NASA is interested this technology. The average person only knows that blockchain has something to do with Bitcoin.

So what is it? What is it used for? Why do we care? In this series of articles, we will look at blockchain technology, which forms the basis for cryptocurrency. We will discuss what it is, how it works, and why it is so highly valued, and then we will talk about how it is used. Our goal in this series is to try to make blockchain and cryptocurrency less… well, cryptic.

Let’s start with some basic vocabulary:

- The blockchain client is a piece of software. This client maintains the blockchain database.

- The blockchain database is essentially a distributed ledger system which allows the end user to participate in transaction.

- Blockchain technology refers to the overall system that uses these pieces.

Blockchain: What Is It?

Blockchain technology uses the blockchain client with the blockchain database to create a system where the addition of data works by consensus of the users.

In other words, it’s a lot like when you order a pizza with friends. Everyone has to agree on what goes on the pizza or nothing does. With blockchain, every data transaction is observed and agreed on by all parties or the data transaction is deemed invalid.

Blockchain allows unique entries to be made in a manner that ensures the information provided is authenticated before entry. Once this is done, the entry is tagged in such a way that any alteration of it afterwards could be easily noted, thus invalidating the change. So, following our pizza analogy, when the bill comes, every person looks over the entire bill and agrees it is right before the bill gets paid.

This is part of what makes it such a solid foundation for cryptocurrencies. Think of it as confidence by consensus. No one blindly trusts anyone but we all trust each other as a collective.

How Does It Work?

Without blockchain, a transaction between two parties—let’s call them Alice and Bob—would need to go through a third party such as a bank to validate that the money changed hands and verify the action occurred on both sides. The third-party charges fees to ensure that this process happens and that at the end of the day everything ends up where it belongs.

Blockchain turns this idea on its head and instead empowers Alice and Bob to complete the transaction without the expense of a third party. You might be asking, how in the world can this happen? Don’t we need someone to make sure Bob doesn’t cheat Alice and vice versa?

Yes and no. We need a safety check but it doesn’t necessarily have to be an individual third party. In this case, our safety check happens to be the network of people using the same flavor blockchain technology that we are.

I’ll get in to different types/flavors of blockchain technology later in this series. For now, let’s just look at the general principles. In our Alice/Bob case, the two agree on a transaction and an amount. This transaction is a block. This block is then transmitted out to all users of the blockchain so that it can be verified.

This does not mean that every person using this chain is privy to everyone else’s private information nor does it mean each user is sitting there waiting to hit an approval button. Instead, the client waits for new transactions to be broadcast to it and in the background handles verification and additions to the blockchain. The details of each transaction are encrypted by the two parties attempting the transaction. We will discuss the encryption in more detail in our article next week.

Once the transaction has been approved, it is officially added by all parties to the transaction database which uses previous the transactions that have been logged to calculate a signature that ensures this new entry is not altered.

At this point, the public transaction shows that the amount previously held by Alice is now in the ownership of Bob. So, when Bob decides to purchase something of his own, those assets are now his to work with.

This Sounds Complicated

The concept is not that tricky but the math behind it can be. The first step of this requires the two parties who want to make a transaction to agree that they know each other and that all the information being added to the block is something they both agree on.

It’s like when you were a kid and you promised to trade Magic cards with your best friend’s brother but you weren’t sure you could trust each other. To make the trade, you brought two friends and he brought two friends to a public location. They all watched you two agree and trade. This meant that he could never come back and say you stole that card from him.

Returning to blockchain, each of the steps involved essentially requires looking at the prior data and using that data along with the new transaction to make a unique mark on the new data before it is accepted. As the transaction takes place, the encrypted details of it and how it fits into the blockchain is shared with the members of the blockchain for verification. This information is shared with everybody that uses this shared log before it gets added. If a consensus is reached that it appears valid, it is added to every blockchain and will later be synchronized to the members that were not available at the time of the transaction so that everybody using that type/flavor of blockchain has a copy of the log.

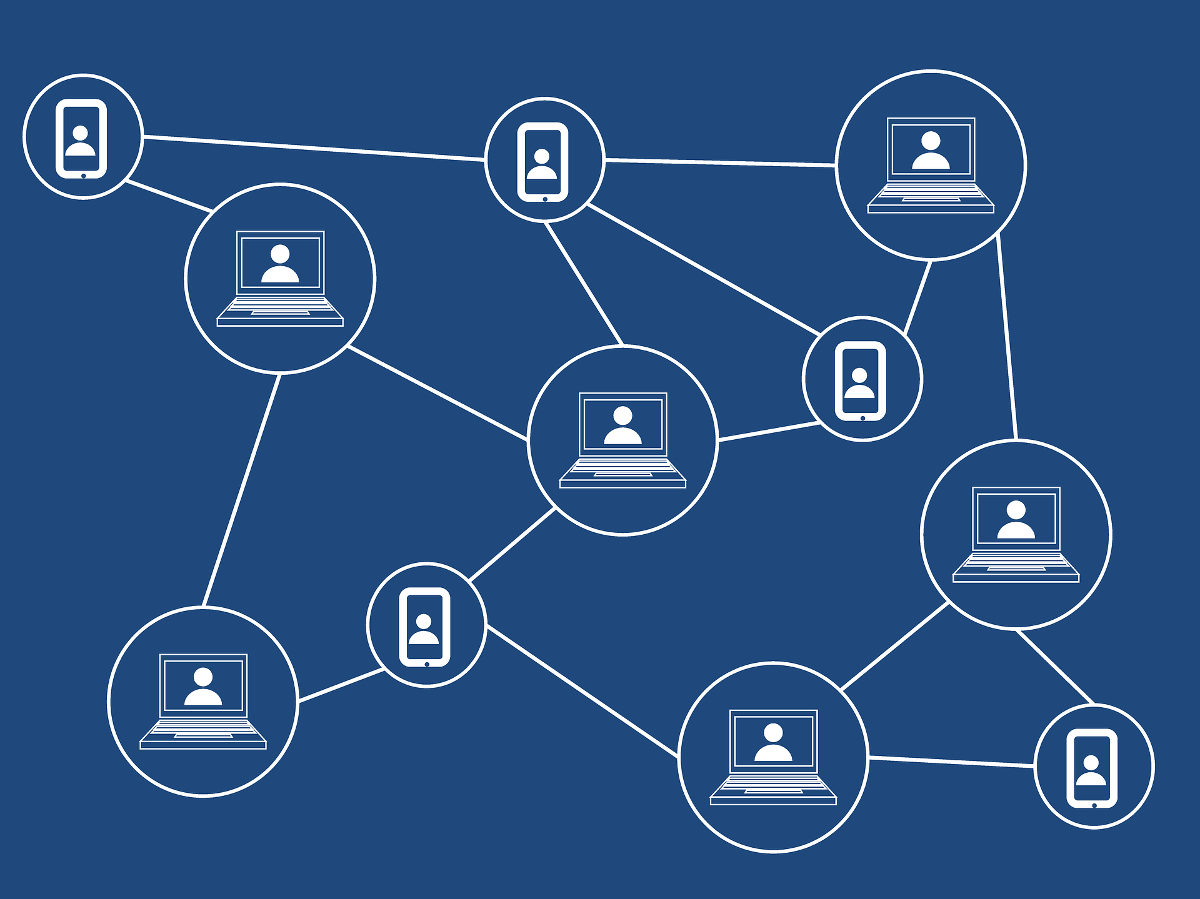

Distributed Ledger

The distributed ledger is a shared log that all the parties using a given flavor of blockchain use. It is a database of transactions that is shared between all the users. It is synchronized in real time as transactions take place throughout the entire user base.

This way the population that utilizes the specific blockchain serves as witnesses to the transactions. It’s not just as simple as they saw the transaction take place, but instead they verify the validity of the transaction using common algorithms to ensure that they all get the same result.

By cross checking each other’s results, they can verify as a group that a transaction is valid and should be added to the ledger. At which point they use previous transactions to create a signature that is applied to the current transaction. This guarantees its spot in the chain.

Is That All?

No, but this should give you a good overview of the basics. Next week we will go into the specific details of how the data is checked off and verified. These are steps that must be accomplished before our transition can be completed. We will also discuss why it is considered more secure. For now, we hope you have a better understanding of the basic concept behind blockchain. Please join us next Monday for the next article in this series.

Thanks, that really helped to clarify the subject for me.

Hi there. Quite interesting post. I recently started working with cryptocurrency trading and I always trying to read such articles to learn more about this business. As I know it can bring good income. With services like godex.io you can easy and fast exchange any coins you need and earn on this!

Hi. Post is very interesting! I think cryptocurrency will never die, especially Bitcoin!

Hey. Quite informative article. It is not so simple to find such relevant information now. I’m interested in cryptocurrency and I want to work in this direction. Recently I found possibility for Bitcoin futures trading, what do you know about this? Looks very promising!

Thank you! This is a good option, as with enough knowledge and practice, you can earn good money. If the first trading experience is successful, then in the future you should analyze the average yield that was obtained when working with a small deposit. Try and learn more about btc scalping. At the initial stage, the main task should be to form a trading discipline and trading strategy!

thank you!

Hello members!) I almost a week just searching for a good way to buy BTC from credit card, do you know some sellers or something?

Business depends on data. The speed of acquisition and accuracy of data are crucial. Blockchain is ideal for providing such information because it offers authorized network members instant, shared and fully transparent access to information in an unchanging registry. I recently learned about whether it is possible to “scalp” cryptocurrency the way people do in forex. It was interesting to read expert opinions.